With policies changing fast in Saudi Arabia (much much faster than long-time watchers ever expected), authorities may have to choose between their overlapping goals including attracting capital, getting the highest valuations for their assets, adding local jobs, involving the private sector, gaining the higher financial and political returns, as well as meet their regional political goals which include countering Iran. In fact, achieving many of the other developments suggest that the involvement of the private sector, at least the local one is the goal that is likely to take a backseat as more and more spending and development is done by government or quasi-governmental bodies. This isn’t in itself necessarily a bad thing or a new thing, as government spending has long been a catalyst for local growth, but it does suggest tradeoffs that will need to be resolved.

The trip may bring to the fore tradeoffs about foreign asset management, local economic goals in both countries and the distribution of returns, but is unlikely to resolve them, and instead is likely an opportunity for MBS to roll out some of the bilateral mercantilist policies that the Trump administration favors (though has struggled to implement with countries like China).

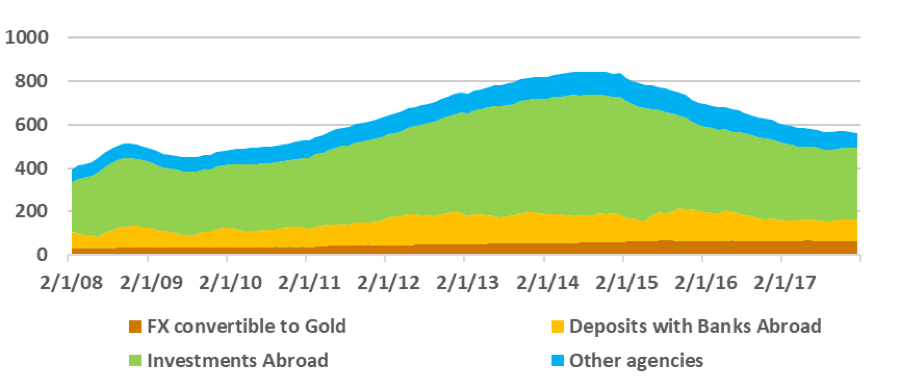

Saudi U.S. Asset portfolio. The Saudi Public Investment fund is the new fund in town and is the key vehicle for diversifying within Saudi Arabia’s USD assets. After a significant drawdown of savings in 2014-6, including some of the US bonds and public equity held by Saudi Arabia, the country’s external accounts are close to balance as the trade surplus is offset by more modest capital outflows. With oil prices now at a level that pays for Saudi Arabia’s imports but doesn’t allow much space for new foreign asset accumulation, Saudi Arabia will be more likely to redeploy existing U.S. funds into perceived higher yielding assets and those that meet its economic agenda. In other words, its holdings of US Treasurys (and publicly traded US corporate bonds and equities) are likely to drop in favor of adding other USD-denominated assets including strategic stakes, a transition that many of its peers in the GCC underwent or at least tested some years ago. This will also include some board stakes and investments that raise additional regulatory scrutiny, not only in the U.S. but elsewhere. In doing so, Saudi Arabia would be following a well trodden path towards more direct investment rather than just investing widely in traded assets.

This tradeoff fuels another one – the split between foreign and domestic investment in the portfolio of the PIF and its role in the broader Saudi investment plan. A sizeable portion of the estimated $200 billion in AUM of the PIF represents domestic pools of capital including those designated for social infrastructure such as education. The PIF is not only quickly scaling up its portfolio of foreign strategic stakes but also is being designated as a primary vehicle for key domestic projects and may be tasked with co-investing with inward investment to Saudi Arabia (like other funds like Russia’s RDIF). This means the organization has to juggle a range of different mandates at the same time. It is thus part of the broad centralized nature of the decision making process in the office of the crown prince and thus may face challenges in interacting with other entities including other parts of the economy ministry, central bank among others.

Fast-moving central implementation vs predictable (decentralized) institutions: A key driver of the fast pace of implementation has been the centralization of policy in the office of the crown prince and his designates, with only a few lead institutions. New entities including the entertainment vehicle, the military investment vehicle have been created. This centralization has prompted a quick moving passage of legislation, but implementation is more challenging given the need to bring the bureaucracy along. A key test case remains the new anti-corruption apparatus and future legal process – establishing clear rules could increase confidence of the local private sector and also foreign investors, many of whom remain concerned about further reprisals despite dismissals from political bodies like the chamber of commerce. Similarly the management of the stakes in companies yielded to the government bodies as part of the last crackdown will be key measures to watch. Centralization of policymaking and the recurrence of the same effective names is nothing new in the gulf, though it takes on a different guide in a country like Saudi Arabia with a larger labor pool to choose from. How Saudi Arabia decentralizes after the past centralization will be key.

The scale of investment including high-profile projects like NEOM and broad localization goals suggest that Saudi Arabia needs to attract foreign portfolio and direct investment capital. Still there may be some capacity constraints in absorbing it even in a country as relatively large and populous as Saudi Arabia (compared to some of the smaller GCC peers like the UAE, Kuwait and even Qatar).

Military and Nuclear equipment: The military ties between Saudi Arabia and the U.S. are long-standing, and have increased in recent years despite a greater push from Saudi Arabia to seek goods from a range of different markets including European and Asian suppliers and to ask all of these producers to consider producing more in Saudi Arabia to meet jobs requirements. With the Chinese piloting some equipment co-investment and transfers, expect the U.S. military contractors to follow suit, though it remains to be seen how many Saudis will be employed. Watch also for the details on any nuclear program – U.S. interests are loath to see it go to an Asian or European competitor but it remains to be seen that congress will support enrichment programs. Negotiations will likely continue just as efforts to “fix” the Iran deal continue. It could be an issue that divides the republican party.

Technology focus and technology transfer: A big part of the U.S. visit includes stops in Silicon Valley, where MBS is likely to check in on existing investments, announce new ones, look to consider new ones and encourage tech companies to set up operations in Saudi Arabia. Many of the existing investments include at least implicit quid pro quo considerations that would encourage local investment. At this point, the focus on the tech investments seems to be primarily about having marquee investments and greater clout with technology transfer secondary. Again this is a key area of diversifying within the USD portfolio. Expect the Saudis to seek assurances that their pledges will be allowed to go ahead in the environment where more tech deals are blocked.

Local issuance goals – for Capital raising or local transfers: While the focus has been on the Aramco IPO, Saudi Arabia is becoming a more major player in EM/Frontier credit and equity may follow. Already in 2017, the GCC, led by Saudi Arabia was one of the dominant USD debt issuers and along with Argentina one of the largest at a time when many countries are focused on local issuance. Although Saudi Arabia and peers are off index (not in the JPM sovereign indices), they are an increasing part of an asset class that has been facing lower issuance. Watch for this to continue in 2018 despite the rise in oil prices, leveraging the interest of USD-tied investors including many in Asia.