Note: As this is a long post, feel free to download it here.

Last week many Emerging market assets came under pressure following the rise in the US 10 year yield. The sell-off was concentrated in Turkish and Argentine markets, whose FX and thus other assets fell sharply, and in USD sovereign debt more generally, but some other assets came under pressure, admittedly falling just outside recent trading ranges. The sell-off prompted a lot of questions about whether this is a broad-based crisis. I don’t think it is? Rather it should be a reminder to look closely at national balance sheets, the quality of growth, fiscal space and resilience.

I’ll try to answer (briefly!) a few key questions in this post: What happened? How have affected central banks responded? How strong are EM fundamentals? Is this another EM-financial crisis (hint: probably not), What would it take for a broader sell-off? what might be the vectors of contagion if it escalated? should we be worried about pegs?

As one would expect given the portfolio effects, which are higher for hard currency debt and equity than local, some other liquid EM saw outflows including Mexico (NAFTA risk), Brazil (election), India and Indonesia (oil and some modest financial contagion) but these seemed modest and are likely to remain so unless there is a meaningful macro risks emanating from China or the U.S. These risks are likely to stay isolated, but add to some growth challenges across relevant regions.

This is unlikely to be the last such bout as investors test the resolve of the Fed to continue normalizing, the significant wave of US bond issuance is absorbed and growth rates stagnate or weaken due to the waning of stimulus and trade policy risks. Higher and rising oil prices – driven by the uncertainties about the Iran deal, continued implosion in Venezuela and profit seeking in Saudi Arabia, only complicate the outlook, causing concerns for oil importing regions and countries, and their consumption and external balance.

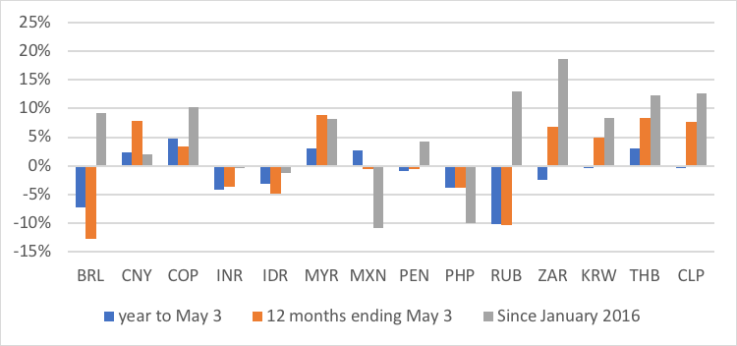

Performance of selected EM FX (% change in period)

Source: Macrobond

Is this just idiosyncratic?

Not entirely, rising rates and USD strength were triggers for reassessment, and we shouldn’t be surprised that countries with weaker balance sheets – large and or growing external and fiscal deficits, high total and FX debt (especially short maturity), inflationary pressures, or who have uncertain policy mix, seem vulnerable (so what else is new?). However as I’ll argue in more detail, broader fundamentals across the EM space, still look decent, inflation is broadly under control, and the credit cycle has slowed in most major EM (a bit of a different story in some frontier markets). Thus, absent a major change in the macro environment – more aggressive stance from Fed, sharper slowdown in China, EM assets as a whole should do ok, but the risk-adjusted reward’s unlikely to be strong.

What’s going on in Turkey and Argentina?

Its little surprise to me that the two countries at the epicenter are among the few with elevated inflation (in double digits), widening fiscal and external deficits, and have some mixed messages from their central banks of late (though Turkey is a much more extensive and repeat offender). Also, recent credit booms, from a low base in Argentina’s case, to fund much needed infrastructure, contributed to fiscal and debt issues, though I tend to think that Argentine officials concede the costs and tradeoffs of their policies (easy fiscal for now, tighter monetary policy). The quality of spending (and what debt finances) are almost as important as the rate of change.

Turkey’s policy mix has been less benign as a massive public credit expansion led to overheating and well-over potential growth last year, which has been deflating. I highlighted Turkey’s status as a “weak link” in my IMF meetings notes, due to the elections, lack of reforms, likelihood of another credit binge and central bank signaling. In particular, it stands out not only for negative real rates and high inflation (low double digits), but also for sizeable fiscal and quasi-fiscal easing, which contributed to a widening of the external deficit and fiscal weakening, which tended to offset vulnerabilities elsewhere.

Turkey, unlike most central banks, uses its range of funding tools to quickly tighten (and then loosen) policy limiting the drag from policy tightening on the economy, but failing to address underlying causes. I’d expect the central bank will not only do some sort of one-off tightening but also address the policy rate. The degree of FX weakening will be an election challenge, and any credit stimulus on course, would make, rate tightening harder.

Argentine policy makers are focused on trying to regain hard-won credibility. The sell-off seemed triggered by an attempt to ease the inflation goals – after defensive hikes and reserves selling. Inflation has been high but stabilizing, but a big infrastructure push (financed largely by debt, with some FDI) fueled imports. The drought only made this more difficult. The central bank, which had been trying to move to a somewhat less tight stance, had to reverse this policy engaging in several sizeable hikes, taking interest rates back up to 40%, a level which is likely to significantly weaken domestic demand. It may be more challenging for them to bring them down than in 2017, though perhaps less politically difficult than the pledge at the end of last week to cut government spending. Overall, the composition of spending is positive, but clarity on the fiscal plan may be needed – this is not the sort of emergency Argentina hoped to face during its G20 presidency.

How Strong are EM fundamentals?

It’s a truism to point to EM differentiation. There is enough diversity of macro drivers – export, commodities, domestic demand and indeed sizeable and growing local investor base across many economies – which tends to limit contagion especially in local markets.

The following factors seem relevant to assess the sort of dollar financing shock: foreign currency liabilities (especially versus trade related inflows), growth trend (relevant for return on equity investments, direct and portfolio), external balance, inflation path and overall overheating risk. Total debt and debt service levels are also key, either capping growth because of servicing costs or risking additional defaults.

Compared to 2013, when US bonds started, prematurely, to price in term premium, several elements of EM balance sheets have improved. Inflation is generally lower (Turkey an exception), external deficits are narrower (as are some surpluses, though maybe not the “right ones), EM FX don’t look massively overvalued, credit growth had ebbed, and few countries have sizeable short-term FX liabilities,. Research that I did last year, while still at Roubini Global economics, suggested that the main area of relative weakness now versus 2013 was in the fiscal position, especially in energy producers, suggesting less scope for stimulus and productivity enhancing investment.

Inflation trends are still benign across most EM, notably so in the commodity producers like Russia and Brazil, which have gone through a period of sharp disinflation following the demand shock from defensive hikes and FX adjustment. While this disinflation looks to be over – notably in sanctions-hit Russia, I see few signs of the credit boom and significant liquidity that would create a major passthrough. Even in commodity importers like India and China, inflation paths are relatively muted, reflecting limited wage growth and constrained credit markets. Indeed, across the EM universe current real policy rates are positive across most countries – and narrowly negative. Turkey and Romania were notable exceptions.

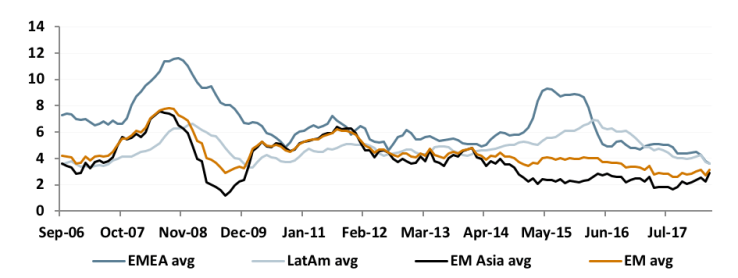

Inflation By Region (% y/y)

Inflation has generally come down, Aside from Turkey

Growth trends have been mixed. Some countries are continuing to exit recessions 2015-6 (Brazil, Argentina, GCC, Egypt, Nigeria), major slowdowns due to policy issues (India, South Africa), while others are slowing due to the end of excessive stimulus (Turkey). The predominant trend in Asia looks to be a moderation closer to potential after a 2017 where global trade growth and supportive FX trends boosted exports (China, South Korea among others), amid decent domestic demand. Going into 2019, EM-DM growth differential should remain steady or grow wider (a trend that is typically supportive of EM assets), though EM average weighted growth should fall.

There has been a structural shift in EM sovereign debt issuance in the last decade or so, with countries that can issue in local currency doing so, and new entrants or those with high local rates dominating USD debt issuance. Indeed, in 2017, Argentina plus GCC/Egypt accounted for over half of the dollar denominated debt issued as many frontier markets steered clear and others chose to issue locally. This shift is important in assessing debt sustainability of these countries as these debt stocks are ratcheting up quickly from a low base.

Still, aren’t there global correlations? What are vectors of contagion?

Common vulnerability to swings in USD/EUR and US yields: USD-denominated debt, especially investment grade and near-investment grade tends to be highly correlated with moves in US yields, first selling off when yields rise and then potentially allowing for some spread compression vs the USD thereafter. IMF research highlights common factors explaining much of hard currency debt movements, vs a much lower proportion for local currency bonds, which tend to benefit from local vested holders. These USD debt also tend to attract more cross-over investors who are choosing between USD denominated assets and may be more fickle. With US HY spreads tighter, there seems to have been more flows into EM bonds to try to pick up further yield. As a result, dollar debt tends to be more linked to global risk appetite. At the same time, greater issuance in the junk segment or near-investment grade, may add to these concerns. Even for local debt, countries with a higher reliance on foreign investors in their bond market, look more vulnerable. A sizeable share of local pensions and institutional investors in countries like Brazil provide cushion. Countries with a sharp increase in foreign holdings may also have more fickle investors.

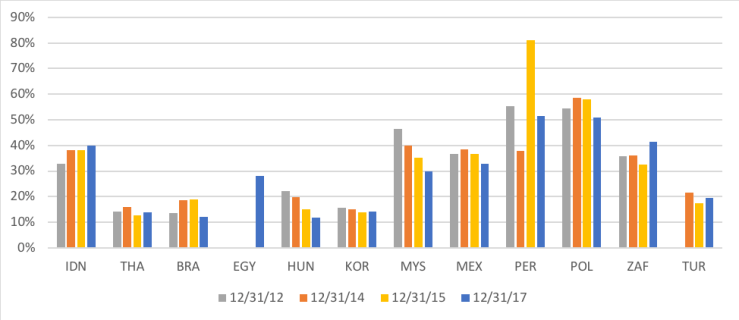

Local currency debt held by non-residents (% of total)

Portfolio construction issues: if investors seek to dump the most vulnerable countries they may also choose to lighten up on more liquid, potentially stronger credits as these are easier to sell. Given the higher correlation between listed dollar debt, this means some countries with stronger credit may still be vulnerable. Should this selling extend to other global assets, it could lead to some greater asset volatility. As more investors access this market via ETFs and other vehicles the impact is likely to increase. However, EM USD debt are still rather small compared to the global stock of USD assets, suggesting the vulnerabilities lie in the other direction. As

Global risk sentiment (vix, S&P500) remains a concern for EM equities particularly for the MSCI EM which does tend to have some correlation. EM valuations still look attractive versus the U.S. which has looked pricey for some time, but some of the cheapest countries (Russia) remain so for a reason.

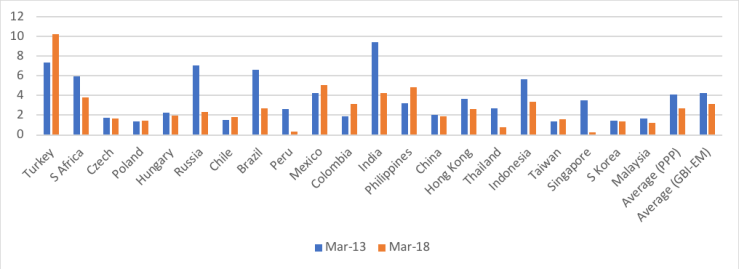

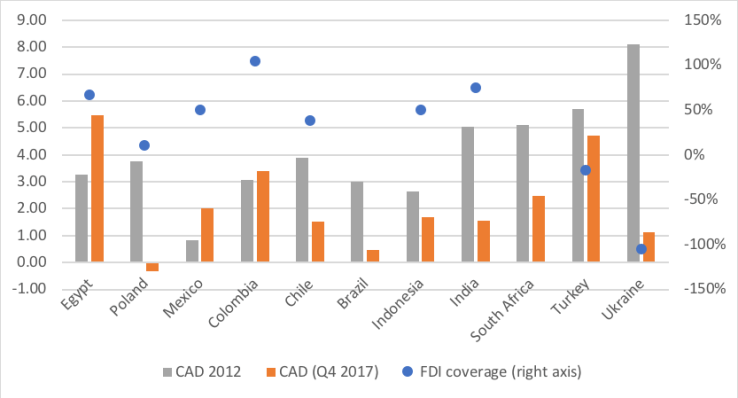

Current account deficit and FDI coverage

Energy prices: local retail fuel prices have risen sharply across EM over the last year and especially over the last two years, helping improve balance of payments for producers (Russia, GCC and to a lesser extent Nigeria) and relieving pressure on the FX pegs in some of these countries. However, global consumers will face some strain from the increase – with India, Turkey and most of Latin America key places to watch. Unlike past cycles, few countries have major fuel subsidy regimes any more – those in Asia were unwound post GFC, and those in MENA (and Mexico) generally in the last few years (though it remains to be seen if prices will rise to full market prices. This suggests that the impact will be felt more through the consumption and external balance channel with the fiscal outlook of importers less constrained.

Growth and global trade: the recent round of leading indicators have seemed consistent with a softening of growth from what has been an above potential pace for the global economy. Global final demand may slow in the coming quarters, especially if the trade policy trajectory makes it more difficult for supply chain planning and dampens investment.

What could change this?

All in all, the signs don’t yet indicate a synchronized slowdown or period of capital outflows. So far outflows have been isolated primarily in the countries at the epicenter. Triggers of a more meaningful crisis are most likely to come from a major economy and could include:

- a more meaningful slowdown in global growth, if for example the recent soft patch shifts to a deeper slowdown. Watch china and the U.S. for signs of this (early warning signs might be visible in Korean and Taiwanese exports/IP which have been weak)

- a sharper Fed hiking cycle, accompanied by a tightening of global financial conditions. So far money and credit trends across DM+ China have shown only a small moderation.

- Significant dislocation from the imposition of sizeable tariffs if the trade bark between the U.S. and China turns to bite (a growing risk as we head towards fall). Two sets of countries look vulnerable to blowback here: surplus countries with sizeable parts in these countries supply chains including South Korea, Malaysia, Singapore, Taiwan and to a lesser extent Philippines and those with USD liabilities and sizeable external deficits that have gotten worse with the oil prices.

- Combination of negative outcomes in several countries – watch Brazilian and Mexican elections with sizeable anti-incumbency bias. While AMLO has taken a pragmatic tone of late, election might still be taken negatively until there is clarity about pricing.

The remainder of this month includes several important policy catalysts, mostly self-imposed by the Trump administration on trade (NAFTA, China) and sanctions (Iran deal). Resolution on the China side seems very unlikely in the near-term suggesting some can-kicking into the summer, but NAFTA timelines are likely to pass in coming weeks, leading to either an agreement in principle (relatively positive for sentiment in the short term).

What about Venezuela? Aren’t they in default? Won’t there be contagion? What about all that debt distress the IMF was warning about last month?

Venezuela remains in a state of default, despite a few payments to bond holders trickling in. The process is likely to be long and arduous, made more complicated by the country’s lack of contact with the IMF, which threatened last week to censure the country, further delaying any possible program if and when the leadership asks for help. Bond holders may still be too optimistic about long-term recovery value, but significant losses are priced in and swings in these bonds have not had much impact on other assets (even countries like Ecuador which historically traded as a proxy). Similarly, the previous unwinding of Petrocaribe energy program to support Caribbean nations suggests limited spillovers to those countries, which aside from Trinidad remain vulnerable to the coming fuel price hikes. Venezuela, sad to say, has done a good job isolating itself to limit financial spillovers – this default has been a LOOOOONG time coming. That said, the humanitarian crisis and costs it is imposing throughout Latin America remain a critical spillover for mostly political reasons. Within key localities the influx is driving up prices and undermining services provision – it may become more of an issue in Brazilian election and impact spending in border areas.

Worth a greater look is debt distress that may be occurring in Zambia and continues in Mozambique. There does not appear to be much spillover in these contexts, but could impact some of the holders of this debt. I would also continue to watch for future reprofilings of the debt of Nigeria and Egypt, which have excessive short-term and costly local liabilities that are being snapped up my foreigners, but those may be issues more for 2019.

What about dollar pegs and dirty floats? Aren’t they vulnerable in this environment?

Yes. With rising US rates and USD strength or even major volatility swings, countries with pegs or quasi pegs tend to be vulnerable. Those most vulnerable are those without sufficient funds to defend the peg or intervention band (few of those remain) and sizeable capital needs (short-term FX liabilities).

After most pegs were broken following the commodity bust (Africa, central asia etc), some have returned to heavily managing their currencies, though most would appreciate, not depreciate if market forces had their way. Questions have been raised about the HKD and the GCC pegs, both of which have been under pressure in the last years. HKD has faced pressure due to the difference between interbank rates and libor, but has more than enough resources to defend. As for the GCC, the sizeable increase in oil prices over the last year provides significant breathing space for the currencies and a new lease on life even for more wobbly balance sheets like Oman and Bahrain. At 70/barrel external balance tilts towards positive (significantly for Qatar, UAE and Kuwait), and suggests moderate external savings. Given that short term FX liabilities are low and reserves slowly being build back up, the pressure should moderate. In fact rising rates may have greater impact on debt service costs in the coming years, even as stronger oil prices make policies only slightly less procyclical.

lovely job you know all this can expand nicely into a good book

you cover the world politics economics interface with the mkts

so good book putting it all together should be good for learning and exposure etc

LikeLike